The Income Tax (Amendment) Act, passed by Ghana’s Parliament in April 2023, amended the Income Tax Act. The act introduced revised income tax rates for individuals, a withholding tax rate on the realization of assets and liabilities, and an additional tax bracket. The amendment also included the introduction of minimum chargeable income, which could be linked to the increase in the National Daily Minimum Wage announced earlier this year by the National Tripartite Committee. These changes were expected to have a significant impact on the country’s economy and workforce.

Following the passage of the Income Tax (Amendment) Act in April 2023, the Ghana Revenue Authority (GRA) announced in a tweet on April 26th that the revised income tax rates and minimum chargeable income would take effect on May 1st, 2023. This means that beginning on the specified date, individuals and businesses in Ghana will be required to comply with the new tax regime. The implementation of the new tax rates, coupled with the increase in the National Daily Minimum Wage, is expected to impact the disposable income of workers and businesses in the country.

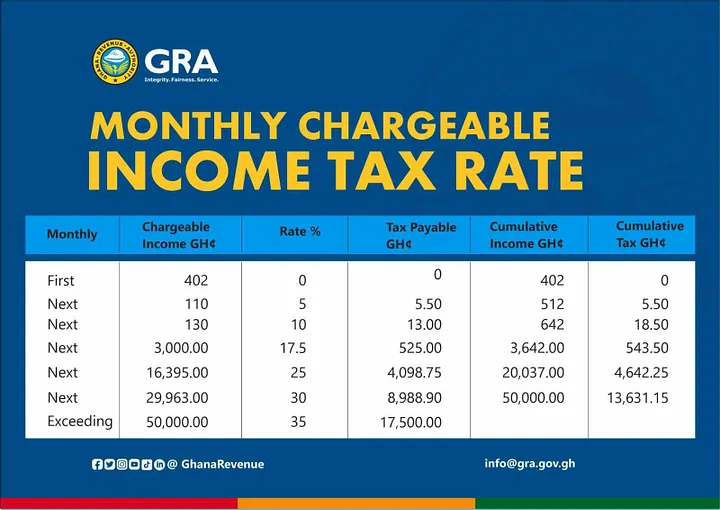

The increase in the National Daily Minimum Wage, which came into effect on January 1st, 2023, has significant implications for businesses and individuals in Ghana. One of the ways in which it affects businesses is by setting the floor for the tax-free band of an employee’s taxable employment income. This means that any employment income earned up to the minimum wage amount will not be subject to tax. Consequently, whenever there is a change in the minimum wage, the Pay-As-You-Earn (PAYE) tax, which is the employee income tax, also changes. This adjustment in tax rates is important for both employers and employees to keep in mind when planning their finances for the year ahead.

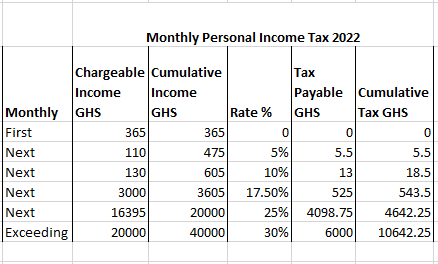

As shown in the above table, previously, the tax-free band for one’s taxable employment income was GHS 365. If someone earned a gross basic income of GHS 1000, they would end up with a net pay of GHS 867 after deducting social security contributions (employee) of GHS 55 and PAYE of GHS 78.

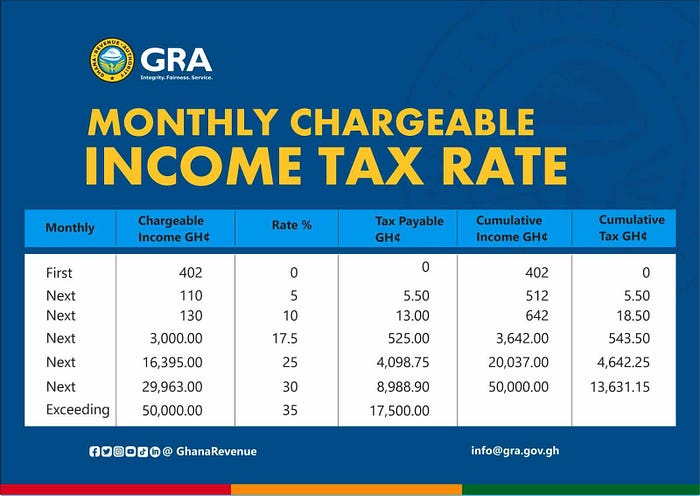

However, with the new rates, the tax-free band for the first taxable income is GHS 402, which is the same amount as the minimum wage. Using the GHS 1000 gross basic income from the previous example, the employee’s payroll figures would be as follows:

Gross Basic Income: GHS 1000

SSNIT (Employee contribution): GHS 55

PAYE: GHS 71.53

Take-home pay: GHS 873.48

In comparison to the previous scenario, the employee’s SSNIT contribution remains the same, but the Pay-As-You-Earn(PAYE) decreases from GHS 78.00 to GHS 71.53, resulting in a higher take-home pay of GHS 873.48 instead of GHS 867.00. This demonstrates the impact of minimum wage changes on employees’ salaries.

To make it easier for you to calculate your PAYE, we have included a template for the current computation that you can download by clicking on this link. Additionally, we have developed a mobile tax calculator app that you can use to calculate both the current PAYE and the new VAT in Ghana.

If you are looking for automated payroll software with all these changes implemented in it, sign up at www.built.africa and start a 30-day free trial. Check out some helpful posts and join the Financial Revolution now!

This is managed by the marketing department

{kind=link}

No Comments